Income tax regulations in India undergo periodic changes, affecting how taxpayers manage their financial affairs. Salaried employees, in particular, benefit from various deductions and exemptions aimed at reducing their tax burden. The old and new income tax regimes offer distinct sets of deductions and exemptions, each with its advantages and implications. In this comprehensive analysis, we will delve into the deductions and exemptions available to salaried employees under both regimes, exploring their significance and providing examples to illustrate their application.

Old Tax Regime:

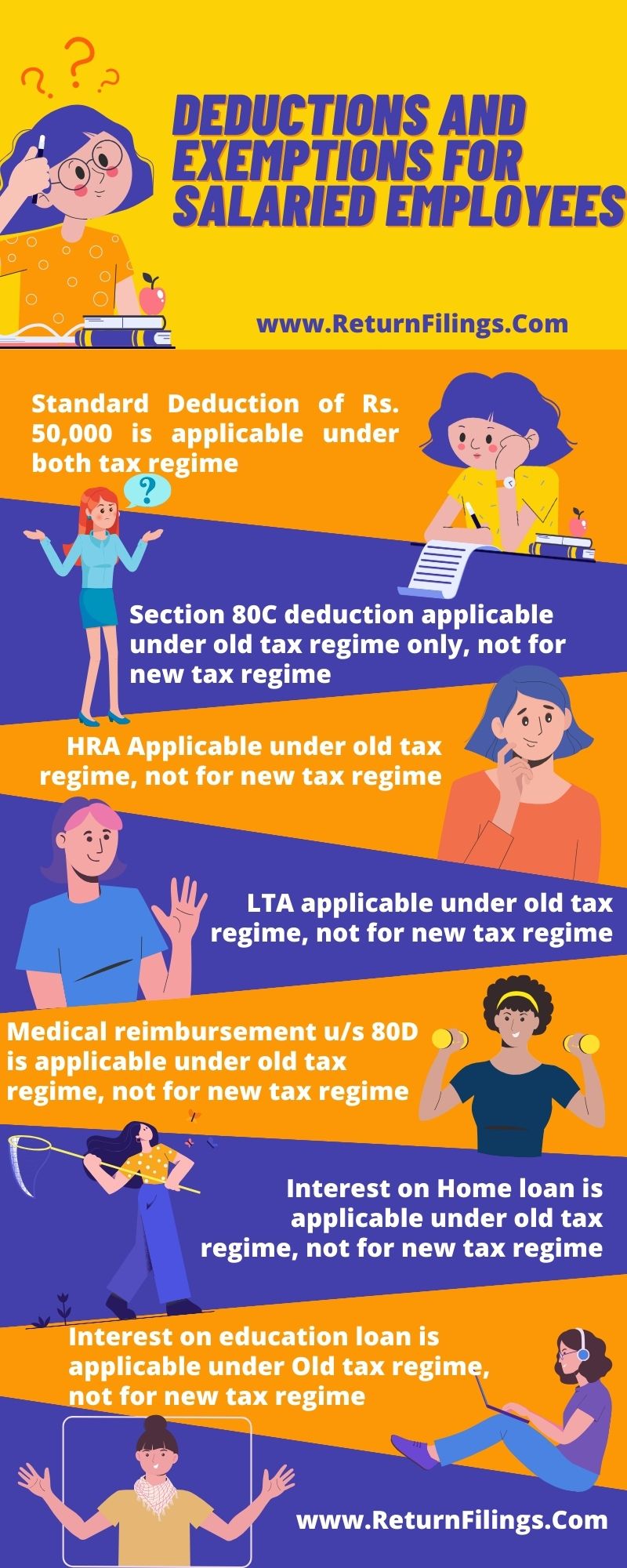

Standard Deduction: Under the old income tax regime, salaried employees were entitled to a standard deduction of Rs. 50,000 from their salary income. This deduction aimed to provide relief from taxes on a uniform basis, irrespective of actual expenses incurred.

Example: Consider a salaried employee earning Rs. 8,00,000 annually. With the standard deduction of Rs. 50,000, their taxable income reduces to Rs. 7,50,000

Deductions under Section 80C: Salaried individuals could claim deductions of up to Rs. 1.5 lakh under Section 80C of the Income Tax Act. Investments in specified instruments such as Employee Provident Fund (EPF), Public Provident Fund (PPF), Equity Linked Savings Scheme (ELSS), National Savings Certificate (NSC), etc., qualified for this deduction.

Example: An employee invests Rs. 1,50,000 in ELSS during the financial year. They can claim the entire amount as a deduction under Section 80C, effectively reducing their taxable income by Rs. 1,50,000.

House Rent Allowance: Salaried individuals receiving HRA as part of their salary could claim exemption under Section 10(13A) subject to certain conditions. The exemption was based on the actual HRA received, rent paid, and the city of residence.

Example: An employee residing in a metro city receives HRA of Rs. 20,000 per month. If their actual rent paid is Rs. 15,000 per month, they can claim exemption on the HRA amount subject to compliance of HRA rules as per Income Tax Act.

Leave Travel Allowance (LTA): Tax exemption was available for expenses incurred on travel within India under LTA, subject to certain conditions and limits. Employees could claim this exemption for travel expenses for themselves and their family members.

Example: An employee undertakes a domestic trip with their family, incurring eligible travel expenses of Rs. 40,000. They can claim tax exemption on this amount under LTA, provided they meet the specified conditions of LTA as per Income Tax.

Medical Reimbursements: Salaried employees were eligible for tax-free reimbursement of medical expenses up to Rs. 15,000 per annum. This exemption aimed to provide relief for healthcare expenses incurred by employees and their families.

Example: An employee submits medical bills totalling Rs. 10,000 for reimbursement under the company’s medical policy. They can claim tax exemption on the entire amount, reducing their taxable income accordingly.

Interest on Home Loan: Deduction up to Rs. 2 lakh was allowed for interest paid on home loan for a self-occupied property under Section 24(b) of the Income Tax Act. This deduction provided significant relief to individuals repaying home loans.

Example: An individual pays Rs. 3,00,000 as interest on their home loan for a self-occupied property during the financial year. They can claim a deduction of INR 2,00,000 under section 24(b), thereby reducing their taxable income by the eligible amount.

Deduction of Interest on Education Loan: Interest paid on education loan for higher studies was eligible for deduction under Section 80E of the Income Tax Act. This deduction encouraged investment in education and provided relief to individuals repaying education loans.

Example: A taxpayer pays Rs. 50,000 as interest on an education loan for their child’s higher studies. They can claim a deduction of the entire interest amount under Section 80E, reducing their taxable income accordingly.

New Tax Regime:

Standard Deduction: Under the new income tax regime, the standard deduction of Rs. 50,000 is applicable. This regime offers lower tax rates but eliminates most exemptions and deduction, however standard deduction of Rs. 50,000 is applicable.

No Deductions under Section 80C: In the new tax regime, there are no deductions allowed under Section 80C. Taxpayers do not benefit from deductions for investments in specified instruments such as EPF, PPF, ELSS, etc.

No HRA (House Rent Allowance) Exemption: HRA exemption is not available under the new tax regime. Taxpayers cannot claim exemption on the HRA received, irrespective of rent paid or city of residence.

No LTA Exemption: LTA exemption is not available under the new tax regime. Taxpayers cannot claim tax exemption for travel expenses incurred within India, even if they fulfil the specified conditions.

No Medical Reimbursement Exemption: Medical reimbursement exemption is not available under the new tax regime. Taxpayers cannot claim tax exemption for medical expenses reimbursed by their employers.

No Interest on Home Loan Deduction: The deduction for interest on home loan is not available under the new tax regime. Taxpayers cannot claim deduction for interest paid on home loans for self-occupied properties under Section 24(b).

No Deduction for Interest on Education Loan: Deduction for interest on education loan is not available under the new tax regime. Taxpayers cannot claim deduction for interest paid on education loans for higher studies under Section 80E.

Conclusion:

The Old and new income tax regimes offer contrasting sets of deductions and exemptions for salaried employees in India. While the old regime provides various avenues for tax savings through deductions and exemptions such as standard deduction, Section 80C, HRA, LTA, medical reimbursement, interest on home loan, and education loan, the new regime offers lower tax rates but eliminates most deductions and exemptions. Taxpayers must carefully evaluate their financial situation and tax planning needs to determine the most beneficial regime for them. Additionally, they should stay informed about any changes in tax regulations to make informed decisions regarding their tax liabilities and savings.

पुरानी कर व्यवस्था बनाम नई कर व्यवस्था के तहत वेतनभोगी

कर्मचारियों के लिए कटौतियों और छूट का तुलनात्मक विश्लेषण

भारत में आयकर नियमों में समय-समय पर बदलाव होते रहते हैं, जिससे यह प्रभावित होता है कि करदाता अपने वित्तीय मामलों का प्रबंधन कैसे करते हैं। वेतनभोगी कर्मचारी, विशेष रूप से, अपने कर के बोझ को कम करने के उद्देश्य से विभिन्न कटौतियों और छूटों से लाभान्वित होते हैं। पुरानी और नई आयकर व्यवस्थाएं कटौतियों और छूटों के अलग-अलग सेट पेश करती हैं, जिनमें से प्रत्येक के अपने फायदे और निहितार्थ हैं। इस व्यापक विश्लेषण में, हम दोनों व्यवस्थाओं के तहत वेतनभोगी कर्मचारियों के लिए उपलब्ध कटौतियों और छूटों पर विस्तार से चर्चा करेंगे, उनके महत्व की खोज करेंगे और उनके आवेदन को स्पष्ट करने के लिए उदाहरण प्रदान करेंगे।

पुरानी कर व्यवस्था:

मानक कटौती: पुरानी आयकर व्यवस्था के तहत, वेतनभोगी कर्मचारी रुपये की मानक कटौती के हकदार थे। उनकी वेतन आय से 50,000 रु. इस कटौती का उद्देश्य वास्तविक खर्चों की परवाह किए बिना एक समान आधार पर करों से राहत प्रदान करना था।

उदाहरण: सालाना 8,00,000 रुपये कमाने वाले एक वेतनभोगी कर्मचारी पर विचार करें। रुपये 50,000 की मानक कटौती के साथ उनकी करयोग्य आय घटकर रु. 7,50,000

धारा 80सी के तहत कटौती: आयकर अधिनियम की धारा 80 सी के तहत वेतनभोगी व्यक्ति रुपये 1.5 लाख तक की कटौती का दावा कर सकते हैं। कर्मचारी भविष्य निधि (ईपीएफ), सार्वजनिक भविष्य निधि (पीपीएफ), इक्विटी लिंक्ड बचत योजना (ईएलएसएस), राष्ट्रीय बचत प्रमाणपत्र (एनएससी), आदि जैसे निर्दिष्ट उपकरणों में निवेश इस कटौती के लिए योग्य है।

उदाहरण: एक कर्मचारी वित्तीय वर्ष के दौरान ईएलएसएस में रुपये 1,50,000 का निवेश करता है। वे धारा 80 सी के तहत कटौती के रूप में पूरी राशि का दावा कर सकते हैं, जिससे प्रभावी रूप से उनकी कर योग्य आय रुपये 1,50,000 तक कम हो जाएगी।

मकान किराया भत्ता: अपने वेतन के हिस्से के रूप में एचआरए प्राप्त करने वाले वेतनभोगी व्यक्ति कुछ शर्तों के अधीन धारा 10(13ए) के तहत छूट का दावा कर सकते हैं। छूट प्राप्त वास्तविक एचआरए, भुगतान किए गए किराए और निवास के शहर पर आधारित ।

उदाहरण: मेट्रो शहर में रहने वाले एक कर्मचारी को रुपये 20,000 प्रति माह का एचआरए मिलता है। यदि उनका भुगतान किया गया वास्तविक किराया रु. 15,000 प्रति माह, वे आयकर अधिनियम के अनुसार एचआरए नियमों के अनुपालन के अधीन एचआरए राशि पर छूट का दावा कर सकते हैं।

अवकाश यात्रा भत्ता (एलटीए): कुछ शर्तों और सीमाओं के अधीन, एलटीए के तहत भारत के भीतर यात्रा पर किए गए खर्चों पर कर छूट उपलब्ध। कर्मचारी अपने और अपने परिवार के सदस्यों के यात्रा खर्च के लिए इस छूट का दावा कर सकते हैं।

उदाहरण: एक कर्मचारी अपने परिवार के साथ घरेलू यात्रा करता है, जिसके लिए पात्र यात्रा व्यय रु. 40,000 एलटीए के तहत इस राशि पर कर छूट का दावा कर सकते हैं, बशर्ते वे आयकर के अनुसार एलटीए की निर्दिष्ट शर्तों को पूरा करते हों।

चिकित्सा प्रतिपूर्ति: वेतनभोगी कर्मचारी 15,000 प्रति वर्ष रुपये तक के चिकित्सा व्यय की कर-मुक्त प्रतिपूर्ति के लिए पात्र। इस छूट का उद्देश्य कर्मचारियों और उनके परिवारों द्वारा किए गए स्वास्थ्य देखभाल खर्चों के लिए राहत प्रदान करना है।

उदाहरण: एक कर्मचारी कुल 10,000 रु. का मेडिकल बिल जमा करता है। कंपनी की मेडिकल पॉलिसी के तहत प्रतिपूर्ति के लिए वे अपनी कर योग्य आय को तदनुसार कम करते हुए, पूरी राशि पर कर छूट का दावा कर सकते हैं।

होम लोन पर ब्याज: 2 लाख रुपये तक की कटौती, आयकर अधिनियम की धारा 24 (बी) के तहत स्व-कब्जे वाली संपत्ति के लिए गृह ऋण पर भुगतान किए गए ब्याज के लिए 2 लाख रुपये की अनुमति है। इस कटौती से होम लोन चुकाने वाले व्यक्तियों को महत्वपूर्ण राहत मिली।

उदाहरण: एक व्यक्ति रुपये 3,00,000 का भुगतान करता है, वित्तीय वर्ष के दौरान स्व-कब्जे वाली संपत्ति के लिए उनके होम लोन पर ब्याज के रूप में 3,00,000 रु., वे धारा 24(बी) के तहत 2,00,000 रुपये की कटौती का दावा कर सकते हैं, जिससे उनकी कर योग्य आय पात्र राशि से कम हो जाएगी।

शिक्षा ऋण पर ब्याज में कटौती: उच्च अध्ययन के लिए शिक्षा ऋण पर भुगतान किया गया ब्याज आयकर अधिनियम की धारा 80ई के तहत कटौती के लिए पात्र है। इस कटौती ने शिक्षा में निवेश को प्रोत्साहित किया और शिक्षा ऋण चुकाने वाले व्यक्तियों को राहत प्रदान की।

उदाहरण: एक करदाता अपने बच्चे की उच्च शिक्षा के लिए शिक्षा ऋण पर ब्याज के रूप में 50,000 रु. का भुगतान करता है। वे धारा 80ई के तहत पूरी ब्याज राशि में कटौती का दावा कर सकते हैं, जिससे उनकी कर योग्य आय तदनुसार कम हो जाएगी।

नई कर व्यवस्था:

मानक कटौती: नई आयकर व्यवस्था के तहत 50,000 रुपये की मानक कटौती लागू है । यह व्यवस्था कम कर दरों की पेशकश करती है लेकिन अधिकांश छूट और कटौती को समाप्त कर देती है, हालांकि 50,000 रुपये की मानक कटौती लागू होती है।

धारा 80सी के तहत कोई कटौती नहीं: नई कर व्यवस्था में धारा 80सी के तहत कोई कटौती की अनुमति नहीं है। करदाताओं को ईपीएफ, पीपीएफ, ईएलएसएस आदि जैसे निर्दिष्ट उपकरणों में निवेश के लिए कटौती से लाभ नहीं मिलता है।

कोई एचआरए (हाउस रेंट अलाउंस) छूट नहीं: नई कर व्यवस्था के तहत एचआरए छूट उपलब्ध नहीं है। करदाता प्राप्त एचआरए पर छूट का दावा नहीं कर सकते, चाहे भुगतान किया गया किराया या निवास का शहर कुछ भी हो।

कोई एलटीए छूट नहीं: नई कर व्यवस्था के तहत एलटीए छूट उपलब्ध नहीं है। करदाता भारत के भीतर किए गए यात्रा खर्चों के लिए कर छूट का दावा नहीं कर सकते, भले ही वे निर्दिष्ट शर्तों को पूरा करते हों।

कोई चिकित्सा प्रतिपूर्ति छूट नहीं: नई कर व्यवस्था के तहत चिकित्सा प्रतिपूर्ति छूट उपलब्ध नहीं है। करदाता अपने नियोक्ताओं द्वारा प्रतिपूर्ति किए गए चिकित्सा व्यय के लिए कर छूट का दावा नहीं कर सकते।

होम लोन पर ब्याज पर कोई कटौती नहीं: नई कर व्यवस्था के तहत होम लोन पर ब्याज पर कटौती उपलब्ध नहीं है। करदाता धारा 24(बी) के तहत स्व-कब्जे वाली संपत्तियों के लिए गृह ऋण पर भुगतान किए गए ब्याज पर कटौती का दावा नहीं कर सकते हैं।

शिक्षा ऋण पर ब्याज के लिए कोई कटौती नहीं: नई कर व्यवस्था के तहत शिक्षा ऋण पर ब्याज के लिए कटौती उपलब्ध नहीं है। करदाता धारा 80ई के तहत उच्च अध्ययन के लिए शिक्षा ऋण पर भुगतान किए गए ब्याज पर कटौती का दावा नहीं कर सकते हैं।

निष्कर्ष:

पुरानी और नई आयकर व्यवस्थाएं भारत में वेतनभोगी कर्मचारियों के लिए कटौतियों और छूट के विपरीत सेट की पेशकश करती हैं। जबकि पुरानी व्यवस्था मानक कटौती, धारा 80 सी, एचआरए, एलटीए, चिकित्सा प्रतिपूर्ति, गृह ऋण पर ब्याज और शिक्षा ऋण जैसे कटौती और छूट के माध्यम से कर बचत के लिए विभिन्न रास्ते प्रदान करती है, नई व्यवस्था कम कर दरों की पेशकश करती है लेकिन अधिकांश कटौतियों को समाप्त कर देती है और छूट. करदाताओं को उनके लिए सबसे लाभप्रद व्यवस्था निर्धारित करने के लिए अपनी वित्तीय स्थिति और कर नियोजन आवश्यकताओं का सावधानीपूर्वक मूल्यांकन करना चाहिए। इसके अतिरिक्त, उन्हें अपनी कर देनदारियों और बचत के संबंध में सूचित निर्णय लेने के लिए कर नियमों में किसी भी बदलाव के बारे में सूचित रहना चाहिए।