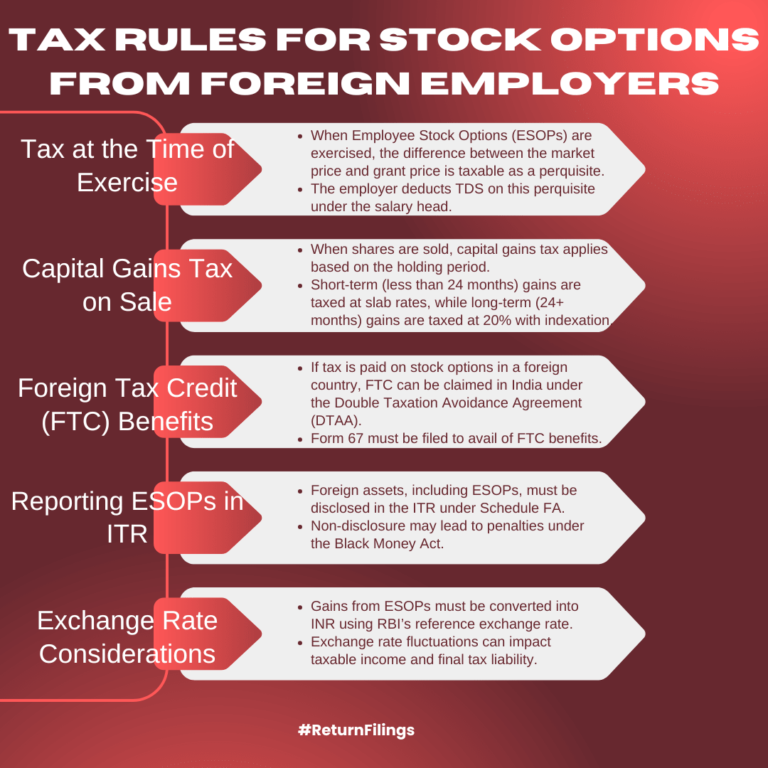

ESOPs are taxed as salary on exercise and capital gains on sale; claim FTC and report in Schedule FA of ITR.

This infographic explains tax rules for Employee Stock Options (ESOPs) from foreign employers. The difference between market and grant price is taxed as a perquisite when exercised, with TDS deducted by the employer. Capital gains tax applies on sale of shares—short-term gains at slab rates, long-term at 20% with indexation. Claim FTC for foreign taxes paid by filing Form 67 and report ESOPs in Schedule FA. Use RBI rates for conversion. Non-disclosure can lead to penalties.