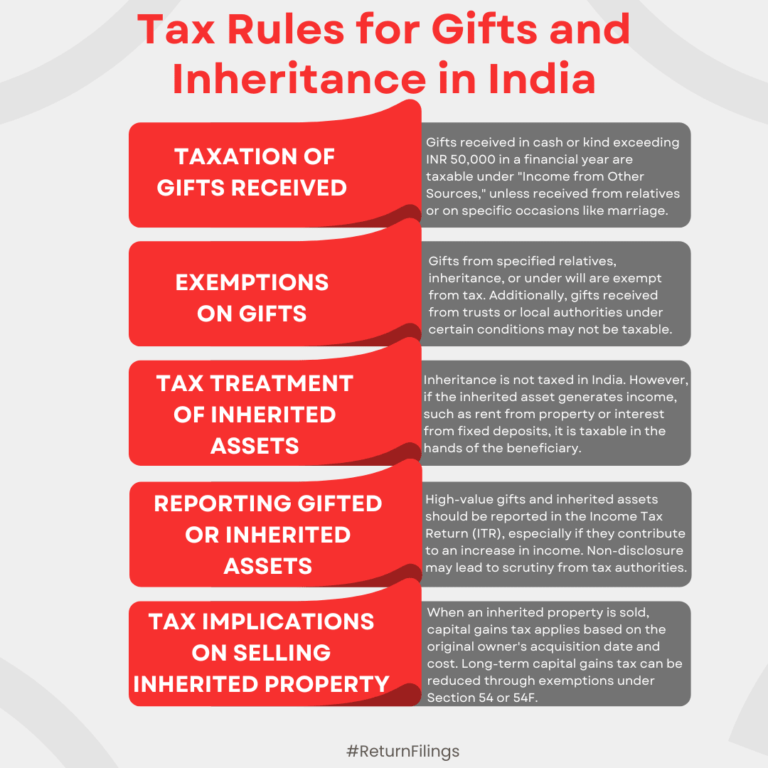

Gifts above ₹50,000 are taxable unless exempt; inheritance is not taxed, but income from inherited assets is taxable and must be reported.

This infographic explains tax rules for gifts and inheritance in India. Gifts exceeding ₹50,000 in a financial year are taxable unless received from specified relatives or on occasions like marriage. Inheritance is not taxed, but income generated from inherited assets, such as rent or interest, is taxable in the beneficiary’s hands. High-value gifts and inherited assets should be reported in the ITR; non-disclosure may attract scrutiny. Selling inherited property triggers capital gains tax, with exemptions available under Sections 54 or 54F.