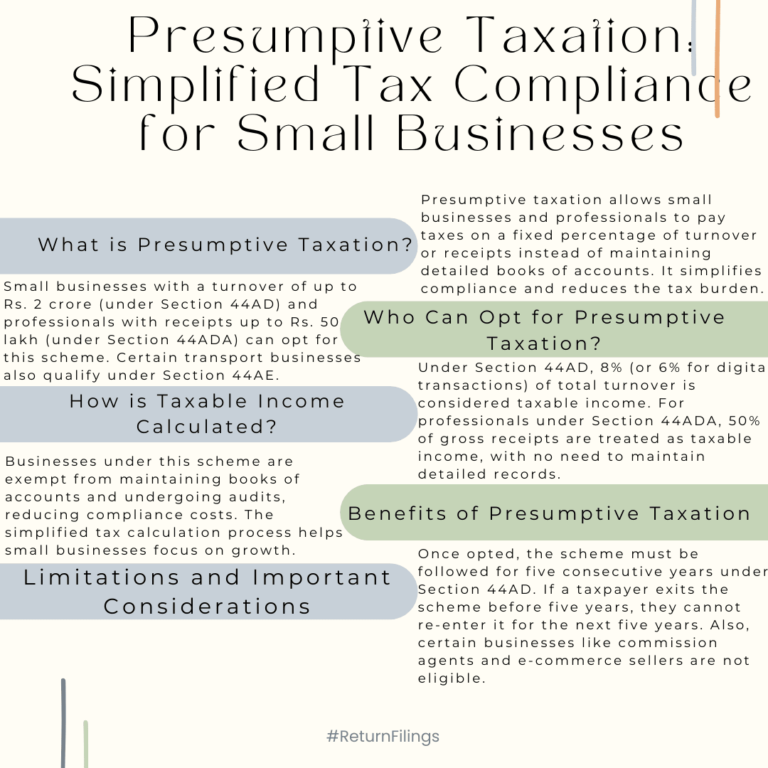

Presumptive taxation lets small businesses pay tax on a fixed percentage of turnover, reducing compliance and audit requirements.

This infographic explains presumptive taxation for small businesses and professionals. Businesses with turnover up to ₹2 crore (Section 44AD) and professionals with receipts up to ₹50 lakh (Section 44ADA) can opt in. Under Section 44AD, 8% (6% for digital) of turnover is taxable; for Section 44ADA, 50% of gross receipts is taxable. No detailed books or audits are required. Once opted, Section 44AD must be followed for five years. Ineligible businesses include commission agents and e-commerce sellers.